The Fiscal Responsibility Act of 2023 was signed into law on June 3, 2023, effectively resolving the U.S. debt ceiling crisis that had unsettled markets for several months prior. While a resolution to this issue is welcome, it raises important questions about potential consequences for the U.S. economy. In Part I of this blog series, we will explore the short-term implications of the debt ceiling, while Part II will delve into the potential long-term impacts of the continuously rising U.S. deficit.

The debt ceiling represents the total amount of U.S. debt that can be borrowed to fund existing government obligations. Obligations include but are not limited to entitlement promises, military payments, and interest payments on existing treasury debt. Without the ability of the U.S. Treasury to raise the debt limit, the federal government would have to rely on incoming revenues, primarily tax receipts, to fund its operations.

On June 3, 2023, legislation was passed to suspend the debt ceiling until January 1, 2025. Modest budget caps were established for defense and non-defense spending, but the most meaningful outcome was the avoidance of a potential U.S. treasury default. [1]

Avoiding a U.S. Treasury Default

If the debt ceiling had not been raised, there was a risk that the Treasury would not have been able to make interest payments on existing sovereign debt. Such a default could have significantly impaired the creditworthiness of the U.S. government, potentially leading to severe economic repercussions, including higher interest rates and the risk of a severe recession. By avoiding a default, market uncertainty is removed and confidence is reestablished. Moreover, the Treasury can assist government operations by regaining the ability to raise debt.

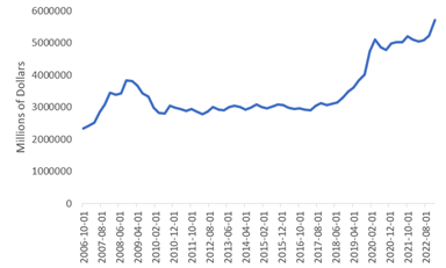

Refilling the Treasury General Obligation Account (TGA)

One of the first orders of business for the Treasury Department is to replenish the Treasury General Account (TGA). This account effectively serves as the U.S. Government's "checking account", where all revenues are collected and expenses are paid. The Treasury issues new debt which is purchased by financial institutions, investors, and foreign governments. The Treasury General Account (TGA) reached dangerously low levels over the past few months due to the Treasury's inability to issue more debt.

Treasury General Account Balance (week avg.)

Figure 1. Source: FRED St. Louis Fed As of 6/14/2023

The TGA bottomed during the week of June 7th with a balance of approximately $44 billion. Estimates predict that the Treasury will need to finance an additional $733 billion from July through September to meet 2023 fiscal year obligations. [2]

One of the key unknowns is how the replenishing of the TGA will affect interest rates and market liquidity in the near term. Short-term interest rates could increase as the market absorbs the additional debt supply issued by the Treasury. Furthermore, bank cash reserves could be utilized to purchase these bonds, effectively leading to tighter liquidity conditions.

How will the market react to tighter liquidity conditions? Will the market be able to digest an elevated treasury issuance in an orderly manner?

A reverse repo is a transaction through which the Fed removes reserves from the banking system by selling government securities to banks or money market funds, with an agreement to buy them back at a higher price at a future date. The operation is effectively a short-dated loan from the financial institution to the Fed. Growth in reverse repo usage has surged due to an increase in excess reserves resulting from the COVID-19 pandemic and the relative attractiveness of reverse repos from a risk-adjusted perspective compared to other short-term securities.

Reverse Repo Growth

Figure 2. Source: FRED St. Louis Fed As of 3/31/2023

Money market funds have absorbed bank deposit assets due to the inability of banks to increase the interest paid on deposits.

Figure 3. Source: FRED St. Louis Fed As of 6/20/2023

An alternative that could potentially neutralize the effect of tighter liquidity, while effectively funding the TGA, is if money market funds exchanged their reverse repos for more liquid Treasury bills. Cash would effectively be exchanged from one “liquidity draining” source to another. However, for money market funds to add T-Bill exposure over reverse repo, they would likely require a higher yield or spread given regulatory and maturity/duration considerations.

Implications on Monetary Policy

The Fed decided to pause hiking interest rates for the first time since March 2022, but left the prospect of future rate increases if elevated inflation stays persistent. The surge in Treasury issuance due to the TGA refill could complicate the Fed's objective of maintaining interest rates within its stated range of 5.00--5.25%. If the new issuance exerts upward pressure on rates, the Fed may need to carry out open market operations to need to expand its balance sheet to manage interest rates and market liquidity, even though it is concurrently aiming to reduce its balance sheet size. The crucial question to consider is whether the Fed will be able to maintain high interest rates and consistent quantitative tightening while the Treasury concurrently refills the TGA.

Ultimately, accurately predicting how market dynamics will be impacted by the suspension of the debt ceiling involves understanding many complex factors. In the second part of this series, we will provide a holistic assessment of the U.S. debt and deficit situation, while also considering the potential long-term effects on the economy, with a focus on interest rates and the value of the U.S. dollar.

Disclosures

Canterbury believes that the information contained herein is accurate and/or derived from sources which are reliable, but Canterbury does not warrant its accuracy or completeness. Canterbury has no obligation (express or implied) to update any or all of the information contained herein or to advise you of any changes. The returns information contained herein is as of the date indicated next to each graphic illustration. Future returns may be higher or lower than the results portrayed in this presentation. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS, WHICH COULD VARY SUBSTANTIALLY. Any references to present or past performance have been provided for illustrative purposes only. It should not be assumed that the strategies represented by these indexes were or will be profitable or that any future investments by Canterbury will be profitable or will equal the performance of the indexes shown.

Sources:

[1] Source: Congressional Budget Office

[2]Source: U.S. Department of Treasury

Mr. Asmus is a shareholder and part of Canterbury’s Research Group. He is responsible for the sourcing, due diligence, and monitoring of public market investment managers. He serves as chair of Canterbury’s ESG, Fixed Income, and Real Assets Manager Research Committees, and vice chair of the Hedge Funds Committee. He also sits on the Capital Markets Committee. Mr. Asmus joined Canterbury in 2013 as an analyst serving institutional and taxable clients. Prior to Canterbury, Mr. Asmus was an institutional fixed income representative for Mutual Securities, LLC, where he provided fixed income solutions for county and city municipalities. Mr. Asmus graduated with a Bachelor of Arts from California State University, Fullerton, where he double majored in business administration, finance, and music performance, jazz studies. He is a CFA® charterholder and a Chartered Alternative Investment Analyst.